Home

»Unlabelled

»

Volatility Smile Skew Smirk / Volatility Skew Definition - In this release, we improved the option analytics panel by adding a list of 37 predefined option strategies that you can apply for analysis or trading with one click.

Volatility Smile Skew Smirk / Volatility Skew Definition - In this release, we improved the option analytics panel by adding a list of 37 predefined option strategies that you can apply for analysis or trading with one click.. But it can also be simpler and ultimately more useful. Implied volatilities are averages of expected future volatilities between spot and strike, between today and expiration. In the wake of the great eastjapan earthquake of march 11, 2011, the japanese stock market. Volatility skew can be used to identify trading opportunities. Define volatility smile and volatility skew.

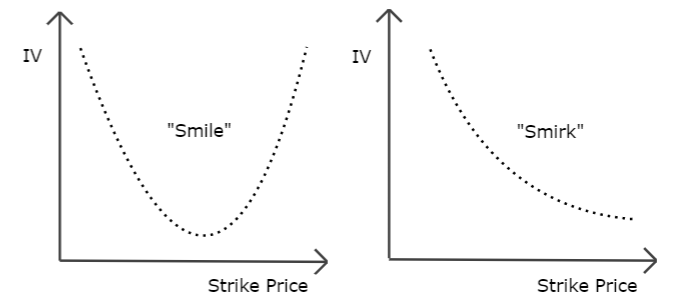

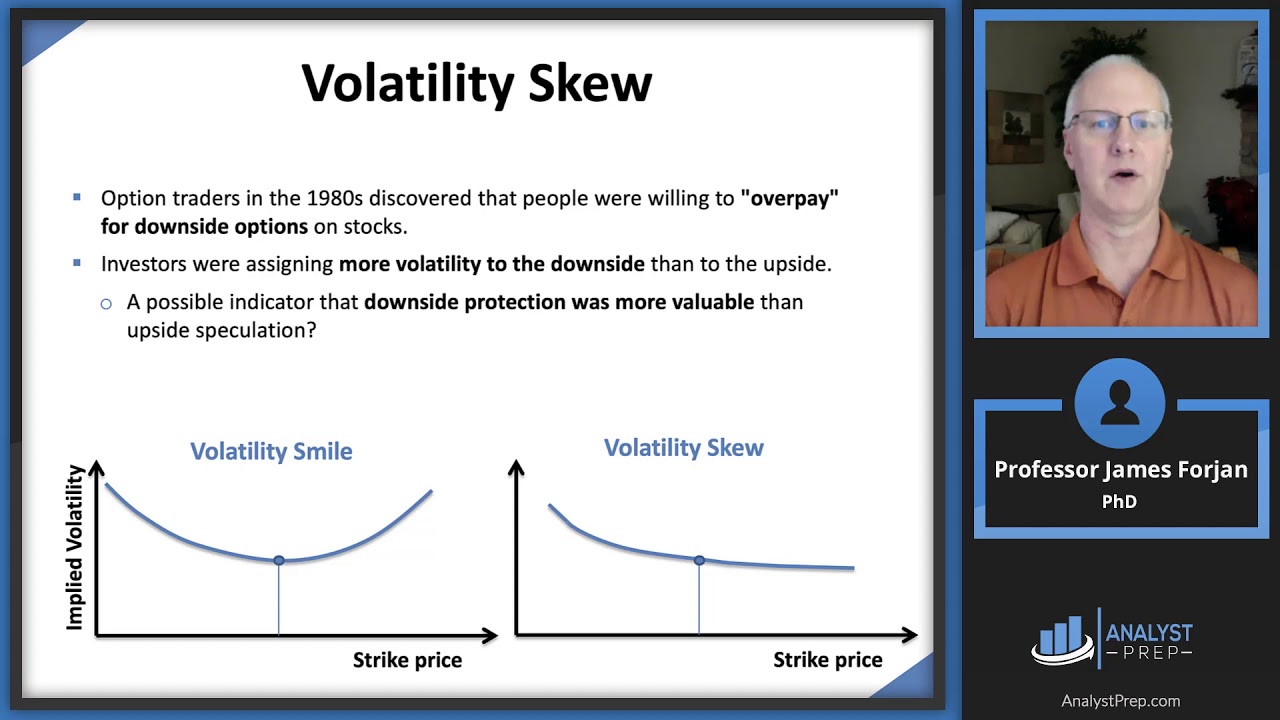

The forward skew is nothing but a reversed form of smirk, in fact, the volatility here tends to become higher for itm puts and otm calls. The reason for the terms 'smile' or 'skew' is that the graph of the implied volatility as a function of the strike price is typically smile shaped or downward sloping. The volatility smile comes from the implied volatility value for each strike within an option's expiration. A skew to a specific strike price can be generated for a number of reasons, but generally it occurs because of higher demand. Cross correlations between volatility level and smirk slope.

Volatility Skew Unofficed from unofficed.com Which products tend to have upside volatility skew? A skew to a specific strike price can be generated for a number of reasons, but generally it occurs because of higher demand. In particular for a given expiration. How to use volatility smile. Ivolatility.com services allow for examination and analysis of the volatility time and volatility smirk often, the shape of the volatility smile for options on shares or an index is called a volatility smirk, because of its ascending line. This chapter takes the fear out of such terms and places them in easy to understand. In my believe this means the overall market. • then figure out the value of the portfolio of vanilla options in a skewed world.

Limitations of using the volatility smile.

If you understand how skew works and you do see that there is an enormous amount of put skew on a given expiration month, it means that those put options are much higher priced. Here, volatility skew refers to implied vols that are different from one strike to the next, or. The volatility smile is one model that an option may align with, but implied volatility could align more with a reverse or forward skew/smirk. The reason for the terms 'smile' or 'skew' is that the graph of the implied volatility as a function of the strike price is typically smile shaped or downward sloping. Evolution of volatility is where volatility charts move from volatility smiles to volatility skews and. Something skewed can be asymmetrical or twisted. A more common skew pattern is the reverse skew or volatility smirk. This is an indicator that measures as you can see, the iv is smirking, and it's a rather steep smirk leaning towards the lower strike puts. A skew to a specific strike price can be generated for a number of reasons, but generally it occurs because of higher demand. When you can't quite manage a smile a smirk will have to do. The implied volatility smile is due to a skew on out of the money options. Implied volatilities are averages of expected future volatilities between spot and strike, between today and expiration. The skew/smirk shows that implied volatility may be higher for either itm or otm options.

Theoretically, the strike prices for an option with the same expiration date should have the same. But volatility skew is an option geek's favorite topic. The skew/smirk shows that implied volatility may be higher for either itm or otm options. The implied volatility smile is due to a skew on out of the money options. Graphical characteristic where the implied volatility of options based on the volatility smile is also sometimes known as the volatility sneer or the volatility smirk.

Volatility Smile And Volatility Skew Part 1 Description Options Trading Beginner from 1.bp.blogspot.com But it can also be simpler and ultimately more useful. Here, volatility skew refers to implied vols that are different from one strike to the next, or. The implied volatility smile is due to a skew on out of the money options. What can volatility skew can tell us? See more of the volatility smirk on facebook. Notably, the smile tends to become less pronounced (and more of a smirk) as the option maturity increases. 153 likes · 1 talking about this. Define volatility smile and volatility skew.

If you understand how skew works and you do see that there is an enormous amount of put skew on a given expiration month, it means that those put options are much higher priced.

Previously, we've talked a bit about volatility smile and volatility skew in this article. Volatility smile — in finance, the volatility smile is a long observed pattern in which at the money options tend to have lower implied volatilities than in or out of the money options. The volatility smile comes from the implied volatility value for each strike within an option's expiration. Ivolatility.com services allow for examination and analysis of the volatility time and volatility smirk often, the shape of the volatility smile for options on shares or an index is called a volatility smirk, because of its ascending line. In particular for a given expiration. This is an indicator that measures as you can see, the iv is smirking, and it's a rather steep smirk leaning towards the lower strike puts. The volatility smile is one model that an option may align with, but implied volatility could align more with a reverse or forward skew/smirk. Daragh mcinerney, agh university of science and technology, krakow, tomasz zastawniak, university of york. Graphing implied volatilities against strike prices for a given expiry yields a skewed smile instead of the expected flat surface. The solution says that the company's stock should be at least $3, then a thinner left tail and fatter right tail than lognormal distribution can be concluded. Here, volatility skew refers to implied vols that are different from one strike to the next, or. I don't know how can these to points be connected? For convenience, all strategies are divided into 4 categories:

Volatility smile — in finance, the volatility smile is a long observed pattern in which at the money options tend to have lower implied volatilities than in or out of the money options. Cross correlations between volatility level and smirk slope. Graphing implied volatilities against strike prices for a given expiry yields a skewed smile instead of the expected flat surface. 153 likes · 1 talking about this. Theoretically, the strike prices for an option with the same expiration date should have the same.

Volatility Smiles Frm Part 2 Study Notes Analystprep from i.ytimg.com What can volatility skew can tell us? Evolution of volatility is where volatility charts move from volatility smiles to volatility skews and. Something skewed can be asymmetrical or twisted. Graphical characteristic where the implied volatility of options based on the volatility smile is also sometimes known as the volatility sneer or the volatility smirk. But volatility skew is an option geek's favorite topic. Graphing implied volatilities against strike prices for a given expiry yields a skewed smile instead of the expected flat surface. Which products tend to have upside volatility skew? Previously, we've talked a bit about volatility smile and volatility skew in this article.

The volatility smile is one model that an option may align with, but implied volatility could align more with a reverse or forward skew/smirk.

The solution says that the company's stock should be at least $3, then a thinner left tail and fatter right tail than lognormal distribution can be concluded. Graphing implied volatilities against strike prices for a given expiry yields a skewed smile instead of the expected flat surface. The skew/smirk shows that implied volatility may be higher for either itm or otm options. Implied volatilities are averages of expected future volatilities between spot and strike, between today and expiration. In the wake of the great eastjapan earthquake of march 11, 2011, the japanese stock market. Volatility smile — in finance, the volatility smile is a long observed pattern in which at the money options tend to have lower implied volatilities than in or out of the money options. I don't know how can these to points be connected? The reason for the terms 'smile' or 'skew' is that the graph of the implied volatility as a function of the strike price is typically smile shaped or downward sloping. Limitations of using the volatility smile. Theoretically, the strike prices for an option with the same expiration date should have the same. This is an indicator that measures as you can see, the iv is smirking, and it's a rather steep smirk leaning towards the lower strike puts. Daragh mcinerney, agh university of science and technology, krakow, tomasz zastawniak, university of york. • then figure out the value of the portfolio of vanilla options in a skewed world.

0 Comments:

Post a Comment